As Manhattan continues to see its revenue rebound following the pandemic, city officials are assessing strategies to manage the city’s rising debt burden.

City Commissioners Tuesday reviewed the 2021 annual report on city finances, as well as the revenue neutral rate and plans for the use of federal American Rescue Plan Act (ARPA) funds.

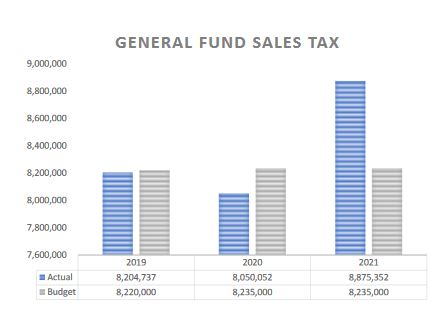

Numerous aspects of Manhattan’s revenue picture last year looked promising to staff. Sales tax revenue was up 10 percent over 2020 and 8 percent from 2019, prior to any COVID-related impacts. Compensating use — i.e. internet sales tax — was up 21 percent over 2020 and 50 percent from 2019. Franchise fees were also slightly up from 2019, having seen a 3 percent growth, while special liquor and transient guest tax revenue both remained more than 10 percent below that collected in 2019.

“Our 2021 numbers are still preliminary and do have the ability to change,” “There are a couple of additional transfers that can potentially happen by the end of March, so we’ll be able to have final numbers by then.”

Overall Manhattan reported collecting 98 percent of general fund budgeted property taxes, on pace with the city’s average over the past half-decade. City Manager Ron Fehr, though, indicated the shortfall seen in 2021 will reiterate or worsen if alternative valuation or ‘Dark Store Theory’ cases continue to see success in winning property tax refunds from the Kansas Board of Tax Appeals.

“You’ve certainly heard us at budget time indicating we should budget for delinquency,” Fehr says. “We should start doing that. We have been sporadically doing that, we don’t necessarily have to do it in every fund but we should do it in some of the major property tax fund.”

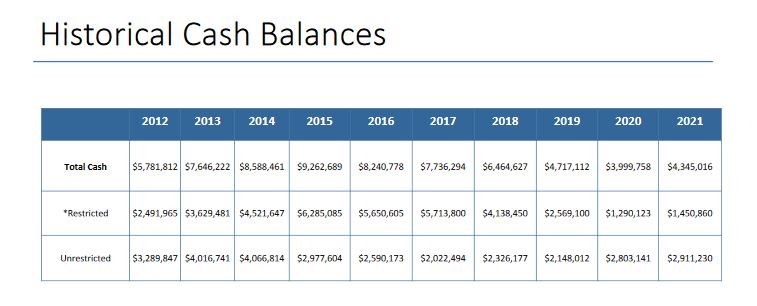

The city’s general fund started the year with a balance of $8.6 million in the general fund, Manhattan’s primary operating fund, on pace with Government Finance Officers Association (GFOA) recommendations for cities of Manhattan’s size. The balance in the bond & interest fund, where the city draws money for debt service for many of its public projects, has become a spot of concern.

“We have been operating at a deficit in the debt service fund for about five years,” says Finance Director Rina Neal. “Meaning we spend more than the revenues that we are bringing in, and the reason why we’re able to do that [is]the reduction in our operating reserves. So we’re using reserves to help balance our debt service fund.”

The balance has trended downward since city revenues began to stagnate in the mid-2010s, dropping from a 10-year peak of $9.2 million in 2015 to $4.3 million in 2021. In that same time, the city’s debt burden has risen substantially as Manhattan undertook a group of major public projects referred to by officials as the “Big Five.” Those constitute Aggieville and North Campus Corridor improvements, the Joint Maintenance Facility construction, the Manhattan flood levee upgrades, and Manhattan Regional Airport runway reconstruction.

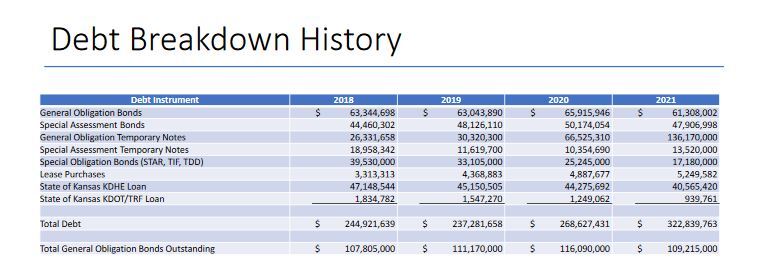

Neal tabulated that Manhattan holds $152 million in general obligation debt, about $40 million shy of the state-imposed limit. That number is up from $88 million as of 2018. With that increased debt load and only $4.3 million in bond & interest reserves where $10 million is recommended by the GFOA, Manhattan saw its bond rating downgraded from Aa2 to Aa3 by rating agency Moody’s as well. The rating indicates how creditworthy a party is, with lower rated cities receiving higher interest rates for projects.

The five projects are timed such that they all are scheduled to be bonded around the same multi-year window, with bond payments starting up thereafter as well. With these all slated to activate after 2025, multiple Manhattan City Commissioners urged caution when considering new projects.

Commissioner Usha Reddi says commissioners need to take a ‘measured’ approach to the prospect of additional projects, with Commissioner Wynn Butler agreeing except in the event of an emergency need.

City Manager Ron Fehr clarified that some debt, such as that related to utility projects, doesn’t count toward the limit and that as the city pays their bills their debt capacity correspondingly expands. Deputy City Manager Jason Hilgers, though, says staff aren’t planning to continue with major projects at the same pace.

“It does require us to measure what it is we’re doing against what we have capacity for and what we can afford.” Hilgers says. “A lot of the approach in the coming years will have to factor this in.”

While the increased interest rates for project adds more to the cost of projects, financial advisor Tom Kaleko of Baker Tilly reassured commissioners that national interest rates remain historically low.

“Project affordability isn’t impacted that greatly,” says Kaleko. “There’s no real reason to panic.

“You’ve been planning at a 4 percent rate, at this point we’re no where close to that so if your model can afford 4 percent you’re sitting in good shape.”

Even so, he says it behooves the city to seek an upgrade in its bond rating and form a plan to handle elevated debt associated with the ‘transformational projects’ occurring around the city. Neal indicated that reducing the city’s debt, generating new revenue and capturing material growth in the community as well as growing the tax base and strengthening the local economy are areas of focus to steer the city back on track and get upgraded back to a better bond rating.

Hilgers says the City Manager’s Office is keeping their eyes on a few sources of revenue to tackle numerous of those, one being the city-wide half cent sales tax that goes into effect in 2023. Butler questioned if they could park that revenue in the bond & interest reserve fund to bolster it in the meantime and bring the balance into the recommended threshold. City officials did something similar with federal CARES money, part of the reason the cash reserves in the city’s general fund are sitting at recommended levels.

Deputy City Manager Jason Hilgers, though, says they plan to create separate accounts for those funds while bolstering reserves a different way.

“Take a four to five year approach, we believe we can get to $10 million by that four to five year approach and have these revenues from the sales tax ready to pay the debt service here.”

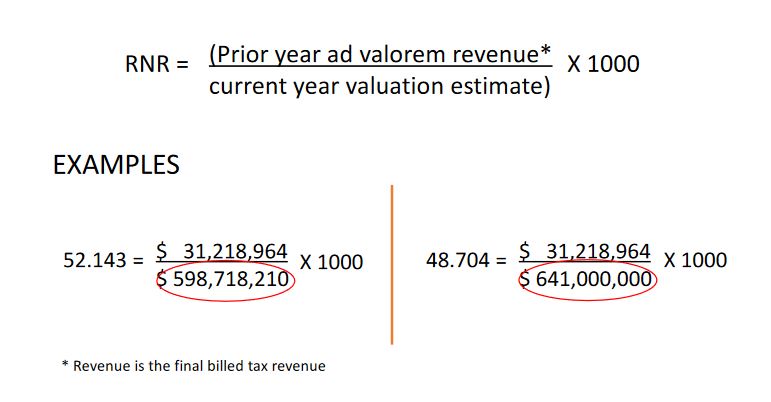

Neal also indicated that property value increases in Riley County would lead Manhattan to exceed its Revenue Neutral Rate if the mill levy were kept flat in the 2023 budget. Riley County appraisers say most properties will see between 10 and 14 percent raises. At a 7 percent increase in valuation, the city’s RNR rate would come in at 48.7 mills — down from the 52.1 levied for the 2022 budget.

The revenue neutral rate calculates the amount of actual dollars generated by a taxing entity the prior year, requiring municipalities to hold public hearings and mail notice to residents.

“It focuses on keeping the impact the same, the dollar amount the same — not necessarily the mill levy the same,” says Fehr. “So if you’re planning to capture any new construction at all to help pay for expanding services then you’re automatically going to exceed that revenue neutral rate.”

More than $88 million in new construction was approved last year, says Fehr, and will require a hearing if commissioners hope to see it grow the city’s tax base.

“I believe we have to capture the growth — it doesn’t make sense not to,” says Butler. “So to me that means you’re going to exceed the RNR, it just is.

“The other consideration is I don’t know what the inflation rate is going to end up being, but I think we’ve got to capture that, too, and this RNR does not allow for that.”

Commissioners also discussed possible uses for ARPA funds Tuesday, with the final rules coming down in January. ARPA dollars have a variety of potential uses, generally intended to replace lost public sector revenue and in response to the impact of the pandemic. Funds are eligible to be used for expenses incurred beginning March 3rd, 2021 – according to federal rules, all funds must be spent by the end of 2026.

“It is only subject to the overarching restrictions on all fiscal recovery funds,” says Kaleko. “Which are you can’t pay debt service, you can’t put it into a reserve fund, you can’t make extraordinary deposits into pension funds and you can’t pay legal judgments and settlements.”

Manhattan is anticipating more than $6.3 million to come down in May. Fehr recommended a community appropriations process if any of the funds are planned to be committed to community service organizations, funding requests from which always exceed the budget available.

Mayor and Law Board Chair Linda Morse advocated for some portion of the funds to go to the Riley County Police Department. The Riley County Law Enforcement Agency Board in September approved letters requesting ARPA funds to cover emergency leave pay and other one-time expenses. Morse’s proposal, though, didn’t elicit resounding support.

“We kept the police department whole by making a full transfer of the budget where we cut our expenses on our side drastically,” says Fehr. “So our first priority is going to be to try to make ourselves whole.”

Morse, though, said it behooves the city and county alike to help the department. She says police departments with more direct local governance structures elsewhere are getting access to the funds, and doesn’t want to leave RCPD out.

“It’s up to us to share those funds in some way,” she says. “And that doesn’t mean making them whole at our expense, it means that we take that into consideration in some way so that they’re not being punished.”

The post Manhattan seeks to bolster reserve funds, manage increased project debt burden appeared first on News Radio KMAN.